“Mr. and Mrs. Recession, where have you been?”

What has happened to date is relatively simple; consumer spending and the labor market have both remained strong. “We are at a fork in the road economically, and the path chosen by the Fed will determine what comes next. Many feel the Fed has stopped raising rates and inflation will drop to acceptable levels without further interest rate increases.

“Others believe the Fed is so adamant about bringing inflation down that they will continue raising rates until they reach their 2% goal. This inflection point is important because if the Fed sticks to the last rate increase, we may have a chance to achieve the “magical” soft landing, which means they reduced inflation without throwing the economy into recession. However, if the Federal Reserve raises interest rates another .25% or more, the likelihood of a recession increases.” (Chairman’s letter summer 2023)

Well, the Fed did not raise rates, and it is looking like a chance for a soft landing, or at the very worst a light recession.

There are still many issues that could throw us into recession—there are always a lot of negatives that could happen—but there are an equal number of things that could keep us out of recession. On October 19, 2023, Federal Reserve Chairman Jerome Powell signaled the central bank could hold rates steady at its next policy meeting, but he also warned that inflation was still too high and that more interest rate increases are still possible if the economy stays surprisingly hot.

“Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy,” Powell said while speaking before the Economic Club of New York. To recap, since March 2022, the Fed has increased rates 11 times.

The debate last fall was whether they would raise rates yet another time; as you may remember, I did not believe they needed to raise rates. But based on my history with the Federal Reserve, I thought they probably would. I give them credit for not raising rates. The Fed had adopted a stance that would keep rates high for as long as needed, indicating they will probably keep rates high for a long period of time. Although inflation has moved down from its peak—a welcome development—it remains too high.

“We are prepared to raise rates further if appropriate and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.” Then suddenly on December 13, 2023, the Fed made a very strong pivot. This is one of the few times that I was caught by surprise. They changed their stance and said they may consider cutting rates sooner than expected. This was good news for the market, but since it was such a surprise I wondered if the Fed saw something I did not see.

Did they see some weakening in the economy that was so strong that they were making this change to try and get out in front of a declining economy? I am not sure what triggered this change; however, it did create some concern. As usual, even an indication that rates may decline is generally positive for the markets. The markets finished strong last year with the Dow up 13.7 % closing at 37,689.54, the S&P 500 up 24.2% closing at 4769.83, the NASDAQ up 43.4% closing at 1511.35 and the MSCI EAFE International Index up 18.85% closing at 2,236.16.

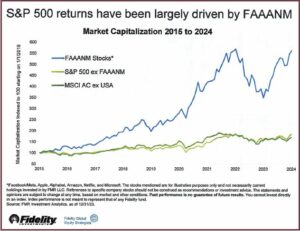

Further, returns from the “Magnificent Seven” made up 76% of the S&P’s 2023 return, but if you factor those stocks out of the S&P 500, it was up 12.5%. At this stage, I think it is very safe to assume that this current cycle of increasing interest rates is over. What about 2024? I always look for quotes which summarize a lot of information quickly and the following are two paragraphs from Barron’s Roundtable January 15, 2024. “It is always a stock picker’s market; however, you must pick the right stocks. If you picked the so-called “Magnificent Seven” last year—a group of highflying, mostly tech stocks that powered the S&P 500 index to a 24% gain—you looked in the mirror and beheld a genius.”

“With a few exceptions, the members of the 2024 Barron’s Roundtable expect the stock market to disappoint, with the index delivering returns of minus 5% to plus 5% for the full year. No, they do not see a ruinous recession, and yes, they expect the Federal Reserve to lower interest rates at some point during the year. Their main worry is that stocks are too richly valued, leaving little margin for error. Those with a sunnier view cite massive capital investment across the economy, the promise of new technologies like artificial intelligence, and incipient investor affection for the less magnificent 493. Bullish or bearish, these 11 money managers and market mavens duked it out January 8 in New York, at a daylong gabfest hosted by Barron’s.”

“While I think this year will continue to be positive for the market, I believe there will be a substantial amount of volatility.”

Individuals and institutions are sitting on a record $5.5 Trillion in money markets: “In the last 50 years the Fed has had 14 tightening cycles. Of those 14, 11 of them the Fed has started cutting rates within five months of the last hike. Taking that a step further, they cut within two months in eight of those 11. The three times they stayed longer than five months preceded the Dot Com Bust, The Global Financial Crisis, and The Pandemic. They are currently in the sixth month.

“When looking to invest, I think it is always good to see what asset classes are out of favor. Regarding what is out of favor, one must look at the International Markets. International has basically been equal to the S&P 494 over the last eight years—dispelling the myth International adds volatility and reduces return.” (Chuck Hutchinson, Fidelity Institutional, Commentary, January 25, 2024.)

After an exhausting amount of reading and trying to analyze a host of competing views and prognostications for 2024 —what do I think? First, when the Fed announced decreasing rates for 2024, the market showed positive returns. The first six weeks of 2024 proved to be even stronger. While I think this year will continue to be positive for the market, I believe there will be a substantial amount of volatility.

What I learned from John Templeton in the 1970’s, was sound advice then and sound advice now. John Templeton, in his book Investing in the Templeton Way, gives the following advice: “Mutual fund investing is identical to doing the same thing in stock purchasing. Both require study, research, and effort, to say the least. “However, once you have gained comfort from your research, you should have the conviction to buy when others are selling, whether it’s a mutual fund or an individual stock.” John Templeton related that exact sentiment to me when I met him in the fall of 1976. This advice also applies to other asset classes besides stocks and bonds.

I am a great believer in investing in those asset classes that are out of favor. Our objective is to try to help you find the best investments and try to keep you from making an emotional investment decision. As you have read many times in this letter, I believe the worst investment decisions are made because of emotions. We are determined to use sound judgment while providing expert guidance to our clients.

In the final pages of Muhammad El -Erian’s book, When Markets Collide, he says the following, “For investors, the to-do list includes the ability to target long-term asset allocations that will play out over time as the new secular realities assert themselves in market prices.”

This is a presidential election year. As most of you know, I love presidential election years. I find the views, strategies, advertising, and all the political trade-offs fasci nating. 2024 will most likely be a positive year for the markets. However, I expect more volatility than we have experienced so far. The caveat being there are a lot of variables, especially international affairs, that could alter what will happen. As I have said many times, it is not what I can see that bothers me, it is what I cannot see that causes me concern.

It is always that variable that comes in from left field that none of us anticipated that I worry about. While I have gone to hundreds of conferences and heard many of the world’s most renowned money managers and economists; I still come back to the basics of how to build net worth. It is really a simple formula. Spend less than you earn, invest the difference wisely, and don’t try to time the markets; instead play the long game. Although I do enjoy election years, this will probably be one of the nastiest campaigns in recent history, and that could add to the volatility.

“Looking back at returns of the S&P 500 for each of the 23 election years since 1928, 17 have ended positively with an average annual return of 7.1%. In addition to that, since 1952, the Dow has climbed 10.1% on average during election years when a sitting president has run for re-election. Politicians recognize the relationship between voter approval and the state of the economy. Sitting presidents often aim to boost the economy just prior to a presidential election, thus garnering voter approval for their re-election and incumbent party.” (“Is the Stock Market Influenced by Presidential Elections?” June 24, 2020).

Going back to the 5.5 Trillion sitting in cash, consumer interest rates are currently high; they will likely go down. The domestic market seems overvalued at the present time so I would not be surprised at a correction. The international markets look very interesting; again, a longer-term approach is needed. Personally, I am going to be buying on dips in this market because I think the market will be higher at the end of the year. Let me emphasize, however, it will be a stressful and bumpy ride to get there.

As always, we are planning several educational events this year and will continue to provide economic and market analysis through periodic webinars hosted by Raymond James. We look forward to meeting with each of you at your financial planning reviews in the office and seeing many of you at our client events in 2024.

Disclaimer: Raymond James is not affiliated with any of the above-named organizations or charitable causes. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material and is not a recommendation. Any opinions are those of Bill Carter and not necessarily those of Raymond James. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Investing involves risk, and you may incur a profit or loss regardless of the strategy selected.

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of Bill E Carter and not necessarily those of Raymond James. Every investor’s situation is unique, and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. There is an inverse relationship between interest rate movements and fixed income prices. Generally, when interest rates rise, fixed income prices fall and when interest rates fall, fixed income prices rise. There is no guarantee that these statements, opinions, or forecasts provided herein will prove to be correct. An investment in a money market fund is neither insured nor guaranteed by the FDIC or any other government agency.

Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the fund. Investors should consider the investment objective, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other important information, is available from your Financial Advisor and should be read carefully before investing. CDs are insured by the FDIC and offer a fixed rate of return, whereas the return and principal value of investment securities fluctuate with changes in market conditions. You cannot invest directly in any index and past performance doesn’t guarantee future results.

Bill Carter founded Carter Financial Management in 1976. The firm has grown to include a full suite of experienced financial planning professionals managing over $1 billion in assets. Dedicated to client service and professional excellence, Bill puts his deep knowledge of tax, investment and estate planning to work in helping clients define and reach their financial and life goals.

Linkedin

Linkedin Facebook

Facebook Twitter

Twitter Youtube

Youtube