Chairman’s Letter – Fall 2022

- Federal Reserve Raises Interest Rates By 75 Basis Points

- Supreme Court Strikes Down New York Gun Law

- 53 Immigrants Die In A Container Truck In Texas

- G7 Economies Show Unity, Agree To Impose A Price Cap On Russian Petroleum Exports

- First Black Female Judge Takes Her Seat On The Supreme Court

- Bipartisan Gun Legislation Passes Into Law

- Supreme Court Overturns Roe V. Wade

- Fed Raises Interest Rates Another 75 Basis Points

- Queen Elizabeth II Dies, And Charles III Becomes King Of The United Kingdom

- Fed Raises Interest Rates For The Third Time By 75 Basis Points

- The War In Ukraine Rages On

It would be hard to find yourself disinterested in the evening news in this environment. I cannot remember a time in recent history when so many major, diverse events happened simultaneously. These headlines represent issues about which many Americans have firm opinions. We will not discuss all these issues here, but I want to touch on a few areas I know you are asking about because of the potential impact on your finances. The top polling subject in many surveys today is inflation. Concern about inflation is well placed, as the most recent numbers show we are seeing the highest inflation rate in over four decades. The Consumer Price Index for August rose 8.3% over the past 12 months. We should all be concerned about that.

Many believe the Federal Reserve waited too long to raise interest rates and now is facing a difficult situation. To bring inflation under control, the Fed had to raise rates and will probably have to take rates higher than would have been warranted if rate increases had started earlier. Rapidly rising rates, however, can throw the economy into a recession. It is a delicate balancing act, and the Fed will be challenged to slow inflation while avoiding a recession.

You may remember that I said you would start reading more about “soft” and “hard” landings in my March white paper. If the Fed raises rates too high, it slows the economy too much and throws us into a recession – the dreaded “hard landing.” Alternatively, if the Fed raises rates just enough to bring inflation under control without throwing the economy into recession, we experience a “soft landing.” Federal Reserve Chairman Powell has stated that he believes a recession can be avoided. He might be correct in this; I am not so optimistic. Speaking to CNN in July, former US Treasury Secretary Larry Summers said “Soft landings represent a kind of triumph of hope over experience.” I feel a soft landing is going to be difficult to achieve. I think we will see continued rate increases, but the Federal Reserve will be very measured in its response to current economic conditions. I would expect rate increases not to be excessive.

At this stage, most economists and money managers I follow expect a “hard landing,” but a soft landing is still possible. The first two 75-basis point increases have already had a significant impact, and the Fed just approved a third increase. We are seeing housing prices begin to level out. The pricing advantage sellers have had over the last few years has quickly evaporated as mortgage rates increased overnight. This slows new homebuyers from entering the market and starts a chain of decreasing demand for more expensive homes, as fewer sellers will be able to progress to their next move upmarket. The housing market remains vibrant, but it is slowing, and costs are beginning to peak. I think this slowdown is a good thing. You know the market is overheated when you see people flipping houses as investments instead of buying homes for their residences.

According to the July 16 Dallas Morning News article, “Housing Hits a Turning Point,“Conditions in the housing market eroded more quickly than anticipated in the past six weeks, according to the Beige Book for the Federal Reserve’s Dallas-based 11th district, which includes Texas and parts of New Mexico and Louisiana. The report, which collects anecdotal information from key business contacts and other sources, said housing sales were off notably from earlier in the year, and online and foot traffic had slowed markedly. Cancellations also rose, in part because of problems qualifying for loans.

Many people have made money in this real estate market; however, the last buyer may not be so fortunate. I continually remind myself that the Dallas market is often different than the rest of the country, as it is usually more stable. According to my real estate contacts, the Dallas market is slowing, as is the rest of the country. In August, D/FW home sales dropped 10% compared to August of 2021, and home inventory rose 68% from a year earlier according to a recent report from the Texas Real Estate Research Center at Texas A&M. Again, slowing in the housing market is positive news from an inflation perspective. Despite more supply, the median home price in the D/FW metro market remains up 15% year over year. I do not feel the real estate market will turn south anytime soon, but I believe the upward trajectory will flatten.

We are already seeing a softness in retail sales and other indications that inflation has probably peaked and will begin a slowing trend. Energy prices, at least at the pump, have started decreasing. While a decreasing gas price is a welcome change, it is important to remember, as I have stated before, that there are over 6,000 products that use petroleum. I suspect most, if not all, of those products have increased their prices, at least partly because of the increase in energy costs. It will take time for those prices to decline, if they ever do.

We are experiencing an unusual situation currently; consumer sentiment is very negative, yet consumer spending is strong. I think there are a few contributing factors: people still have disposable dollars resulting from a diminished Covid lifestyle, and stimulus money has not yet been entirely spent. The considerable number of people traveling demonstrates that people still have disposable dollars. Trends show costs are not a significant factor to people taking vacations. People are still traveling despite price increases across the board for gas, air transportation, food, and hotel accommodations. The American public has been isolated for nearly two years and is determined to go on vacations and excursions, regardless of cost, it would seem.

There is also still a great deal of liquidity in the economy. For example, according to an article in the Dallas Morning News on July 24, $18 billion in approved Texas school district federal aid is still largely unspent. Texas schools have tapped less than a third of that cash due to supply chain delays, staffing shortages, and trouble hiring factors that have tripped up spending plans. School leaders may need to rush to use all funds before the 2024 deadline.

Volatility in the markets will continue until we reach the mid-term elections or until the results of those elections become evident. The market could turn positive before then, as the market is a forward predictor. Inflation coming under control, economic growth stabilizing, and job growth staying steady could spur the market to turn around sooner than people expect. You have seen this before.

Many years ago, when I was a young planner, I asked an old sage during a bear market, “When does the market stop declining?”

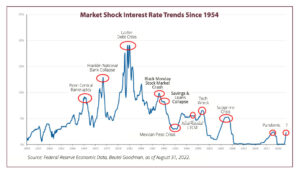

His response was simple: “The market stops declining when there are no sellers.” He explained that once selling stops, the market will stabilize. It may not turn upward for some time, but the market decline will end, as has repeatedly happened during my 50-year career. Typically, bear markets end with a capitulation; in other words, there is a massive sell-off as investors lose confidence in the outlook for stock prices and begin “panic selling.” Capitulation is notable because it often signals the end of declines, as investor sentiment can’t get much worse from that point.

Some believe a capitulation occurred on June 17, 2022, when the Dow reached the 2022 low of 29,888. The S&P 500 fell to 3,674, a 23% decrease from the beginning of 2022. By the end of June, the S&P 500 had posted its worst half since 1970. Maybe there won’t be another capitulation—but there could be, and I don’t want you to be surprised if it happens. I don’t think we’ve seen the end yet. Rising rates make stocks less attractive, and markets have shown jitters in anticipation of additional rate hikes. We’ve had drops recently, but we are still above the June Dow low. If another sell-off does occur, it may be the finale of this current downward cycle in equities. I don’t think we’ve seen the final capitulation event yet.

The Fed tool that has yet to drive results is quantitative tightening, which removes liquidity from the economy. This strategy is the opposite of quantitative easing used during Covid-19 to stabilize the economy. I think this tightening could impact as much, if not more, than an increase in interest rates.

At some point, when the market determines the Fed has raised rates high enough to bring inflation under control, the markets should stabilize. Of course, the timing is impossible to predict, but I think there is still a possibility we will see the economy, interest rates, and the stock market level out later this fall. I still believe there is a chance for a late-year stock market rally.

In August, Senator Joe Manchin made front-page news when he reversed his position on supporting a scaled-down version of the Build Back Better bill. A consultant I follow closely said recently that Senator Manchin had specific items he expected in the bill. If the “powers that be” would accept his changes, including putting revenues toward reducing the nation’s debt, he would support the legislation. His demands were met, resulting in the Inflation Reduction Act of 2022. The bill was signed into law August 12, 2022.

Like any legislative bill, there are both negatives and positives. While I think some of the spending is excessive, I do like the fact that “carried interest” is being eliminated, which hedge fund managers have significantly used to their advantage. The downside to the bill is a potential tax increase that will affect many folks read- ing this letter. Generally, raising taxes in the face of a looming recession is not wise. If this legislation passes, the question becomes, “is our economic growth strong enough to overcome the tax rate increases?”

Looking ahead, I am optimistic. I believe the economy is strong and will stay strong. Many problems that plagued growth over the last two years, from Covid to supply chain issues, will begin to subside. While I think consumer spending will decrease somewhat, I do not think it will drop significantly.

This year’s Carter Investment Conference was on September 13, 2022. It was great to see so many faces live again. We were fortunate to have some excellent speakers. Jeff Bush and his firm have previously been as accurate as any consulting firm in the country regard- ing elections and election results. Our other speakers on energy and infrastructure were also terrific. Whether you attended live or via Zoom, we appreciate your support and hope you left feeling prepared for what is ahead.

As always, we will continue to follow events very closely, so feel free to call your planner at any time to get our current thoughts and assessments. I hope you have managed the heat as we have gone through a summer with record-breaking temperatures; cooler weather is another reason to look forward to this fall.

Sincerely,

Bill E. Carter, CFP®, CLU®, ChFC® Chairman and CEO

Carter Financial Management

Any opinions are those of Bill Carter, CEO, Carter Financial Management, and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. The information contained in this report does not purport to be a complete description of the travel insurance industry referred to in this material. It has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary and does not constitute a recommendation.

Becky has been a CFP® professional for over 30 years and has focused her career on helping companies build successful, customer-focused businesses. She has special expertise in financial planning, insurance and mortgage strategies for the retirement marketplace.

Linkedin

Linkedin Facebook

Facebook Twitter

Twitter Youtube

Youtube